{kind=link}

Roth IRAs are fashionable and highly effective, and whereas they’ve an earned revenue requirement, they don’t have a minimal age requirement. So long as a toddler has “official” earned revenue, they will contribute that right into a Roth IRA (technically a Custodial Roth IRA as a minor, with full rights once they flip 18).

There have been varied suggestions floating round on how mother and father may help “assist” the creation of earned revenue for his or her baby. There was even a now-defunct web site referred to as 1417power.com that will “rent” your youngsters to take surveys on-line (in fact, the guardian needed to “rent” 1417power.com first…).

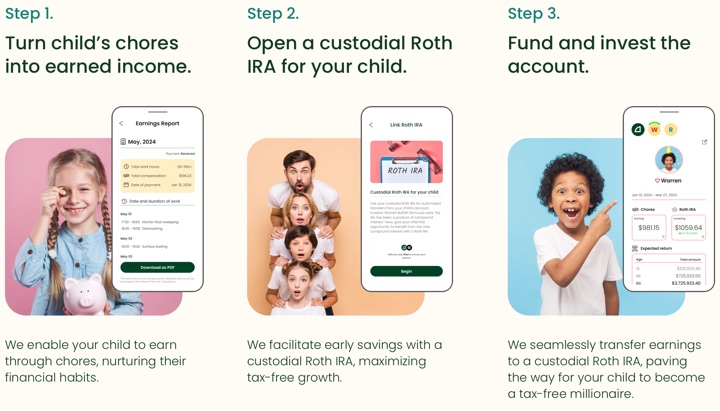

A brand new app referred to as Halfmore can now facilitate the creation of a pleasant paper path between mother and father as employers and youngsters as employees. They promise to show chores right into a Roth IRA steadiness. Based mostly on their screenshots, examples of such chores embody ground sweeping, washing the dishes, floor dusting, and plant watering. The screenshots additionally recommend a pay price of $15 to $16 an hour.

For chores to be acknowledged as authentic sources of revenue, your youngsters ought to be paid for duties you’ll usually rent one other neighborhood child or a nanny to do (relatively than for normal household chores). They need to even be applicable to your baby’s age and talents. Examples embody cleansing the storage, mowing the garden (with out a machine), and babysitting. The work have to be actual, and the wages ought to be truthful.

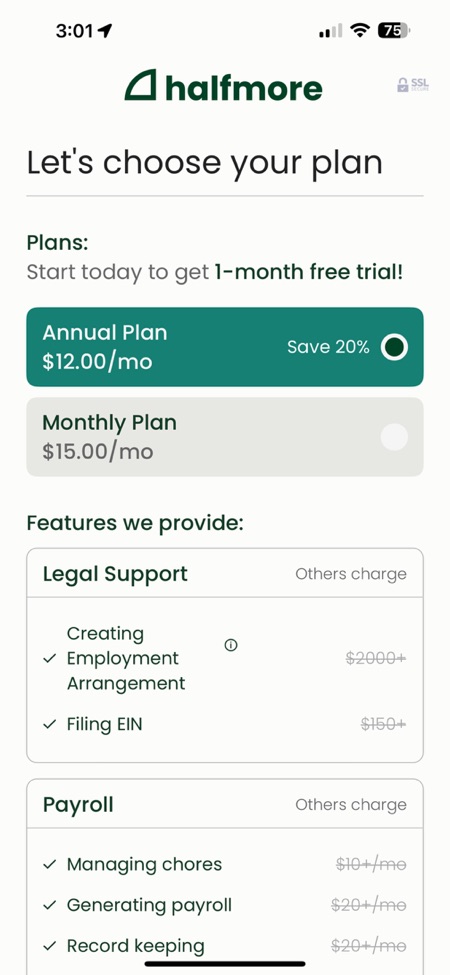

From what I can collect by means of the restricted data on their web site (I needed to register to get extra particulars), that is what they provide:

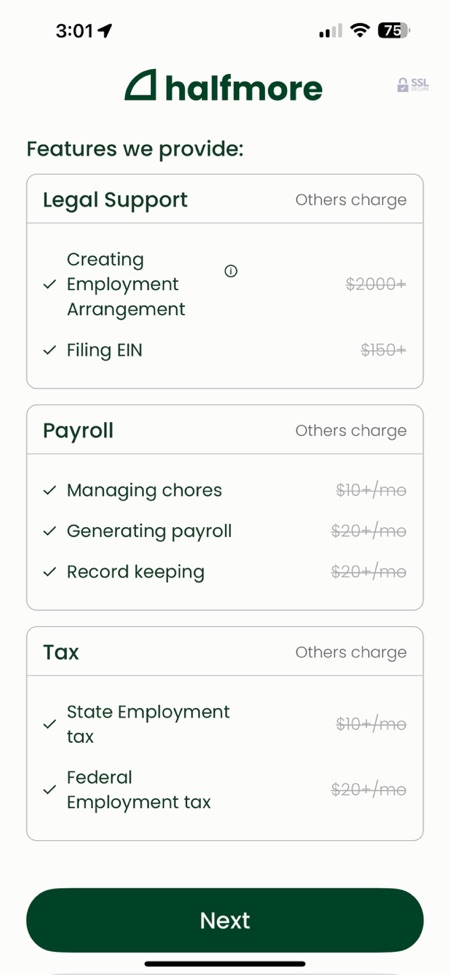

- They are going to enable you to file for an EIN from the federal government, so you might be registered as an official family employer. That is principally the kind of factor you must do in case you employed a full-time nanny.

- By means of the app, you’ll be able to monitor the completion of chores and handle payroll to your youngsters. For instance, the washing of dishes could be marked down as half-hour of labor.

- They are going to put together work documentation for IRS revenue tax submitting and record-keeping necessities.

- They are going to enable you to navigate Federal and State employment taxes.

- They are going to assist open a custodial Roth IRA for you at Constancy or Schwab, and switch cash into that account.

The associated fee is $15 per 30 days or ($144 per 12 months). Their FAQ says this covers as much as three youngsters (one other place on the web site says as much as 5 youngsters). You may file for an EIN, monitor chores, and open up a custodial Roth your self for “free”. You’re basically following the identical steps as in case you had been hiring a full-time nanny as a family employee. However in case you make sufficient cash such that you’re contemplating this scheme to your youngsters, then your hourly price might be excessive sufficient that the comfort issue makes this an inexpensive payment.

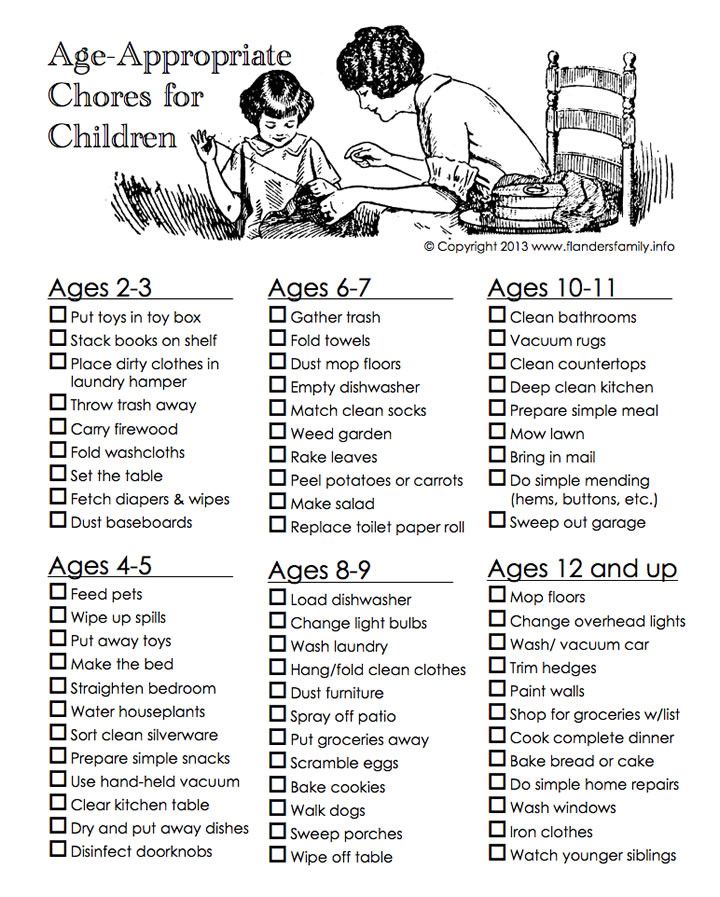

In case you want extra chore concepts, right here is the Montessori Chart of Age-Applicable Chores For Children that retains floating round like a meme:

Wanting by means of my archives, I spotted that I’ve already written about “Roth IRA for Children” in 2007, 2012, and 2019. My eldest baby is in center college now, and I’m nonetheless engaged on learn how to greatest educate them about cash. I can see an identical program in a while in life once they have an actual job from an outdoor employer. However proper now, I don’t pay them something to do their chores. Chores usually are not a job, they’re a duty to their household. They will’t decline their chores by declining the cash. Perhaps I’ll pay for additional jobs round the home, however I feel it’s gonna be a stretch for that so as to add as much as hundreds of {dollars} a 12 months.

In case you already plan on gifting your baby cash anyway, this could be a extra environment friendly methodology. For me, I already inform them that we spend some huge cash on their schooling proper now, and that’s our “present”. I’m already paying loads for tutoring, swim classes, tennis classes, STEM camps, and many others. To not point out who is aware of how a lot school will value! I suppose I simply really feel like that is too far down the record. Perhaps my perspective will change later. Perhaps I’ll simply allow them to have the sense of accomplishment from funding their very own retirement accounts. 😁