THIS POST MAY CONTAIN AFFILIATE LINKS. PLEASE SEE MY DISCLOSURES. FOR MORE INFORMATION.

{kind=link}

In search of a better approach to develop your cash with out playing it away?

Whether or not you’re saving for a down fee, constructing an emergency fund, or simply need your money to do greater than sit in a financial savings account, you’re not alone.

Many individuals are asking the identical query: The place can I park my money brief time period with out taking massive dangers?

The excellent news?

There are alternatives – low threat investments that provide strong returns with out locking up your cash for many years.

When you’re seeking to develop your cash safely over the subsequent 1 to five years, these choices could be just right for you.

On this information, we’ll discover a number of the finest brief time period funding choices accessible proper now.

Whether or not you’re simply getting began or need to fine-tune your monetary plan, this text will provide you with actual, actionable concepts that can assist you make your cash work more durable – with out the stress.

The ten Greatest Quick Time period Investments For Your Cash

| Funding Kind | Benefits | Drawbacks |

|---|---|---|

| Excessive Yield Financial savings Account | -Quick access to funds (extremely liquid). -FDIC insured (as much as $250,000). |

-Rates of interest can fluctuate. -Decrease returns in comparison with different investments. |

| Financial institution CD | -Assured mounted return. -FDIC insured. |

-Early withdrawal penalties. -Decrease liquidity (locked-in for a time period). |

| Dealer CD | -Entry to larger CD charges by varied banks. -Will be offered on the secondary market (extra versatile). |

-Could promote under authentic worth if cashed out early. -Not all brokerage CDs are FDIC insured, relies on the issuing financial institution. |

| Cash Market Accounts | -Larger curiosity than normal financial savings accounts. -Verify-writing and debit card entry (in some instances). |

-Could require a excessive minimal steadiness. -Rates of interest not as aggressive as some on-line choices. |

| Financial savings Bonds | -Backed by the U.S. authorities. -Tax-deferred curiosity till redeemed. |

-Should be held for at the very least 1 yr (not liquid). -Penalty if cashed earlier than 5 years (lose 3 months’ curiosity). |

| Treasury Payments | -Very low threat (government-backed debt securities). -Extremely liquid and simple to promote. |

-Decrease yields in comparison with riskier investments. -Curiosity is topic to federal earnings tax. |

| Spend money on Small Companies | -Larger charge of return than different choices. -Potential to take a position spare change. |

-Potential to lose cash. -Rate of interest may drop sooner or later. |

| Spend money on Actual Property | -Larger charge of return than different choices. -Can make investments with as little as $10. |

-Can’t promote for six months. -Redemption price if offered inside 5 years. |

| Quick Time period Bond Funds | -Diversification throughout a number of bonds -Potential for larger returns than .financial savings accounts or CDs. |

-Not insured, worth can fluctuate. -Rate of interest threat (worth could drop if charges rise). |

| Peer 2 Peer Lending | -Potential for larger returns. -Helps particular person debtors or small companies. |

-Larger default threat (not insured). -Funds could also be tied up for the mortgage time period (decrease liquidity). |

#1. Excessive Yield Financial savings Accounts

The most secure place to place your cash is a conventional financial savings account at your financial institution or credit score union.

The issue with these accounts is that they pay little to no curiosity.

So whilst you don’t lose cash as a result of the cash you set in is protected, you do lose on the subject of buying energy.

For instance, if you’re incomes 1% in your financial savings and inflation is 4%, your cash is rising slower than costs are rising.

If in case you have $100 saved, in a single yr you’ll have $101. However one thing that prices $100 at present will price $104 in a single yr.

As you’ll be able to see, you didn’t lose your cash in your checking account, however you might be falling behind on the subject of maintaining with inflation.

The excellent news is that many banks and credit score unions provide excessive yield saving accounts.

These are the very same as a traditional financial savings account besides that they pay larger rates of interest.

Since most banks provide these accounts, it’s worthwhile to discover a financial institution that isn’t solely reliable, but additionally pays a excessive rate of interest.

You don’t need to merely select the financial institution with the best charges as oftentimes these could be teaser charges that can drop shortly.

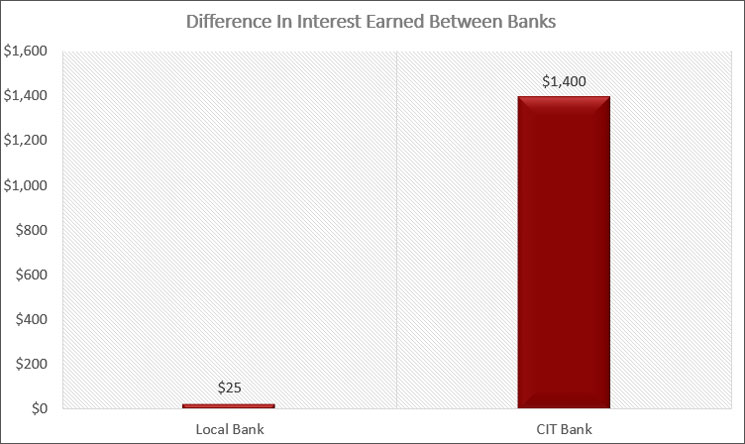

One in every of my favourite banks is CIT Financial institution.

Greatest Financial institution Account

CIT Financial institution

With one of many highest paying rates of interest within the U.S. CIT Financial institution stands out as one of the best excessive yield financial savings account. Add in ease of use and nice customer support, and you’ve got a transparent winner.

We earn a fee should you make a purchase order, at no extra price to you.

This financial institution provides a web based financial savings account with an rate of interest that’s traditionally one of many highest within the nation, permitting you to earn much more curiosity.

They usually persistently rank on the high of the listing of highest curiosity paying accounts on a regular basis.

Present Charge You Can Count on to Earn: Between 4.25% and 5% relying on the financial institution

#2. Financial institution Certificates of Deposit

Investing in a certificates of deposit (CD) is an effective way to earn the next rate of interest in your cash.

The distinction with a financial institution CD is the potential for larger curiosity, also referred to as yield.

In return for this larger yield it’s important to lock your cash up for a time frame.

With a financial savings account, you might be free to take your cash out of the account everytime you need.

However with a CD, you could have a time frame that it’s important to depart the cash within the account.

You already know the size of this time period since you select the time period.

Commonest CD phrases are 6 months, 1 yr, 18 months, 2 years and 5 years.

The longer you lock your cash up, the upper the rate of interest you’ll earn.

After all, if you actually need the cash, you’ll be able to nonetheless shut the CD early and get your a refund.

However by doing this, you’ll sometimes forfeit 3 months value of curiosity funds.

Be aware that there are some CDs that provide no penalty should you shut the CD early, however they pay a barely decrease rate of interest due to this.

Lastly, there are some CDs that provide the choice to extend your rate of interest one time throughout the time period.

Since your rate of interest is locked while you open the CD, you could possibly lose out if rates of interest rise with a typical CD.

By letting you enhance your charge one time, you’ll be able to decrease the probabilities of this threat.

Present Charge You Can Count on to Earn: Between 4% and 4.50% relying on the time period

#3. Brokerage Certificates of Deposit

You can too purchase a CD by your dealer, like Schwab or Constancy.

Doing this provides two fundamental advantages: larger curiosity and extra liquidity.

Most CDs you should purchase by a dealer provide the next rate of interest than from a financial institution.

After I was investing in these CDs a couple of months in the past, a 6-month financial institution CD was paying 4.5% whereas a dealer CD was paying 5.25%.

The opposite profit is which you could promote your CD at any time on the secondary market.

This can be a fancy means of claiming there are traders at all times searching for CDs and in consequence, you’ll be able to promote your CD earlier than maturity.

There is no such thing as a penalty for doing so, however rates of interest will decide how a lot or how little you’ll be able to promote it for.

Present Charge You Can Count on to Earn: Between 4% and 4.75% relying on the time period

#4. Cash Market Accounts

Cash market accounts, or cash market funds, are a means so that you can earn larger curiosity with out locking your cash up like with a certificates of deposit.

There are 2 varieties of cash market accounts.

The primary is just about the identical as a financial savings account.

The one actual variations are that you just have a tendency to want the next steadiness within the account, for instance $25,000 or extra and you’ll write checks on the account.

Banks can pay the next rate of interest on a cash market account since you might be depositing more cash.

The second sort of cash market account is a cash market mutual fund.

These accounts put money into short-term financial institution devices and a few brokers name them a money administration account as a result of you’ll be able to deposit cash, write checks, and in some instances, have a debit card.

The underlying worth of the cash market fund stays at $1 (though again in 2008 after the housing collapse, some funds did “break the buck”).

Basically, with a cash market fund, your cash is protected and you’ll earn a bit extra curiosity than a primary account on the financial institution.

Present Charge You Can Count on to Earn: Between 3.60% to 4.50% relying on the financial institution

#5. Financial savings Bonds

Financial savings bonds are one other brief time period funding choice.

Whereas sometimes thought-about long run investments, you need to use these authorities securities within the brief time period.

Financial savings bonds are backed by the total religion and credit score of the federal Authorities and are subsequently thought-about freed from default threat.

At present there are two varieties of financial savings bonds accessible for buy, the EE Collection and Collection I.

The distinction is how they pay curiosity.

- EE Collection financial savings bonds pay a set charge of curiosity. The speed you earn is ready while you buy the bond, and stays fixed for the lifetime of the bond.

- I Bonds pay mounted charge of curiosity, plus an adjustable charge. The rate of interest on an I Bond is made up of two parts, a set charge element and a floating charge element. The mounted charge element on an I Bond is ready when the bond is bought and stays fixed for the lifetime of the bond. The floating charge element is reset each 6 months and is predicated on the present stage of inflation.

The rate of interest on an EE Collection financial savings bonds is decrease than what you can find with lots of the different choices listed right here.

However there are some fascinating issues to think about.

First, should you hold your EE Bond for 20 years the federal government ensures that it’ll at the very least double in worth.

If you do the maths, this comes out to a return of three.5% over the lifetime of the bond.

This works as a result of should you money in your bond after 20 years and it isn’t value double the acquisition value, the federal government will make an adjustment to the ultimate worth of the bond so it will likely be value double what you paid.

The second fascinating factor to think about is that whereas you’ll owe federal earnings tax on the curiosity you earn on the bond, you’ll not owe any state earnings tax.

Lastly, you’ll be able to keep away from taxes altogether through the use of the bonds and the curiosity to pay for larger training.

The identical tax advantages of the EE bonds are true for I bonds as nicely.

Lastly, you’ll be able to money in a financial savings bond at any time after holding the bond for 1 yr.

Nonetheless, should you money the financial savings bond in earlier than holding it for five years, then it’s important to hand over 3 months value of curiosity.

After 5 years you’ll be able to money the bond in at any time with out penalty.

Additionally remember that a person should purchase as much as $10,000 value of EE bonds and $10,000 value of I bonds in any given yr.

Present Charge You Can Count on to Earn: Round 3%

#6. Treasury Payments

Treasury Payments, generally often known as T-Payments, are brief time period debt securities issued by the U.S. authorities.

They’re thought-about one of many most secure investments accessible as a result of they’re backed by the total religion and credit score of the U.S. Treasury.

T-Payments are sometimes offered in phrases starting from a couple of days to 1 yr, making them supreme for traders searching for short-term, low-risk alternatives.

T-Payments are bought at a reduction to their face worth, and traders earn a return when the invoice matures and the total face worth is paid.

For instance, you may purchase a $1,000 T-Invoice for $980 and obtain the total $1,000 at maturity, with the $20 distinction being your earnings, or the “curiosity” you earn.

As a result of there are numerous patrons for these authorities bonds, they’re extremely liquid, permitting you promote at any time.

Present Charge You Can Count on to Earn: Between 4% and 4.20% relying on the time period

#7. Make investments In Small Companies

Earlier than I advised you how one can earn 192% extra curiosity by opening an account with CIT Financial institution.

Right here I’ll do you one higher.

You’ll be able to earn near 200% extra curiosity by buying Worthy Bonds.

What are Worthy Bonds?

It’s an funding that has your funding loaned out to small companies to fund their stock wants.

In addition they assist fund actual property tasks as nicely.

Worthy costs a low rate of interest to the small enterprise after which Worthy turns round and provides you 7% in your funding.

By investing with Worthy Bonds, you earn 7% in your cash.

Greatest Method To Earn Passive Earnings

Worthy Monetary

Trying to safely earn the next return in your cash? Worthy Bonds provides 5% 7% curiosity in your cash. Spend money on small companies and earn a return for doing so. New customers get a $10 bonus when buy your first bond.

We earn a fee should you make a purchase order, at no extra price to you.

The catch is there may be some threat to your funding.

In reality, that is the primary brief time period funding that does put your principal in danger.

Perceive although that this threat is small.

Worthy is required to have a contingency fund of cash in case a small enterprise doesn’t pay again their mortgage.

On this case, Worthy would use the cash within the contingency fund to pay you the 5% in your financial savings.

In different phrases, Worthy Bonds has an emergency fund to guard traders.

The chances of this occurring nevertheless are slim for the reason that firm goes to nice lengths to mortgage cash out to prime quality companies.

Moreover, the loans are backed by the stock of the small enterprise.

You will get began with Worthy Bonds with as little as $10. You’ll be able to even arrange your account to take a position your spare change.

This works by having Worthy spherical up your purchases to the closest greenback and make investments your spare change to purchase extra bonds.

When you common $500 in spherical ups a yr, in 10 years you’ll have an extra $6,600!

Present Charge You Can Count on to Earn: At present 7% till January 2026, then 5%

#8. Spend money on Actual Property

I’m a giant fan of investing cash in actual property.

The issue is you want sufficient cash for a down fee to purchase a property.

And should you plan to lease it out, there may be a number of work there, except you rent a administration firm, after which there may be an added price.

To sidestep this, I’ve been investing with Arrived.

It’s a crowdfunding platform that swimming pools traders cash and buys properties.

Then quarterly, I earn a dividend primarily based on my share of possession.

I additionally earn a return when the appreciated property is offered.

The explanation Arrived is a brief time period funding choice is due to their Non-public Credit score Fund.

Best Method To Make investments In Actual Property

Arrived Properties

In search of a straightforward approach to get began investing in actual property with out some huge cash? Look into Arrived Properties. Decide the only household homes within the components of the nation you need to put money into and earn passive earnings.

Begin Investing In Actual Property

We earn a fee should you make a purchase order, at no extra price to you.

This fund invests in short-term loans to fund actual property tasks.

At present you earn round 8% and make investments with as little at $10.

The drawboack of this concept?

It’s not essentially the most liquid funding as a result of it’s important to hold your cash locked up for at the very least six months earlier than you’ll be able to promote, and there’s a price should you promote in lower than 5 years.

Present Charge You Can Count on to Earn: At present 8%

#9. Quick Time period Bond Funds

The subsequent brief time period funding to think about is brief time period bonds.

The primary distinction with brief time period bonds over the opposite concepts talked about is that that is the primary one that you’ve got the next threat dropping principal.

In different phrases, should you make investments $1,000 briefly time period bonds, you could possibly find yourself with $900 or much less.

So far as the rate of interest brief time period bonds pay, all of it relies on total charges and what the Federal Reserve is doing.

However earlier than you run off to purchase brief time period bonds, it’s important to perceive how they work.

With out complicated you utterly, know that when bond costs rise, rates of interest fall.

And when bond costs fall, rates of interest rise.

For instance, take a bond that’s promoting for $100 and yielding 3%.

If charges rise to three.25%, the worth of the bond will drop under $100. Whilst you lose principal, you do earn extra curiosity.

Perceive that I like to recommend investing in bond funds over particular person bonds as it’s simpler and more economical.

One of the simplest ways to put money into brief time period bonds is thru ETFs and mutual funds.

By investing briefly time period bond funds, you purchase a basket of bonds at varied costs and rates of interest, diversifying your threat.

You additionally purchase bonds with varied maturity dates.

This can be a fancy means of claiming when the bond ends and the investor will get their principal funding again.

An excellent portfolio to put money into would include the next bonds funds:

- iShares Quick Treasury Bond ETF (SHV)

- iShares Extremely Quick-Time period Bond ETF (ICSH)

- iShares 0-5 12 months Funding Grade Bond ETF (SLQD)

By creating this portfolio of curiosity paying bonds, you’ll earn an OK yield and has the potential to supply development of your principal as nicely.

Present Charge You Can Count on to Earn: Between 5% and 6%

#10. Peer To Peer Lending

One other decrease threat choice is to trying into peer lending, or p2p lending.

That is the place individuals who want cash crowdfund their mortgage by skipping the financial institution.

Right here is the way it works.

Let’s say I want $10,000 for a automotive.

I’m going in Lending Membership or Prosper and after doing a background test on me, these websites enable my mortgage to be posted for funding.

You see my mortgage and the rate of interest you may be paid and determine to take a position $200.

Assuming others make investments sufficient to hit my $10,000 purpose, the mortgage is made.

Now each month for the subsequent 5 years you’re going to get a portion of your $200 funding again, plus curiosity.

The rate of interest varies by mortgage and borrower and you’ll construct a portfolio of investments by investing in a handful of loans.

Present Charge You Can Count on to Earn: Between 5% and 9%

Benefits And Drawbacks

After all with any funding, there are benefits and downsides.

That is true with the varieties of brief time period investments I listing above.

Benefits

- Secure principal. Usually, you received’t be risking your principal while you make investments for the brief time period.

- Simple to foretell. Since your principal is protected and you understand the rate of interest you’ll earn, it’s straightforward to do the maths to see how a lot cash you’ll find yourself with.

- Flexibility. It’s straightforward to get your cash while you want it, and never have it tied up long run.

- Small funding. You’ll be able to usually begin placing cash in these monetary merchandise with as little as $1.

Drawbacks

- Decrease returns. As a result of the investments are usually protected, they pay decrease returns.

- Taxes. On the subject of bonds, you might be paying strange earnings tax charges should you put money into a taxable account.

- Many choices. This can be a profit besides if too many decisions makes it more durable so that you can determine on one funding.

- Curiosity Charge Threat. The largest threat you face when seeking to generate profits over the brief time period is fluctuating charges. Relying on how charges transfer, you may earn much less cash, or with some funding concepts, lose a few of you preliminary funding.

Investments to Keep away from

When investing for the brief time period, there are some investments you need to keep away from, principally as a result of the chance of dropping cash is simply too nice.

The primary is with particular person shares.

Whilst you can earn a excessive charge of return, there may be an excessive amount of threat of dropping cash, particularly should you want the cash in a single yr or much less.

One other funding to keep away from is company bonds.

Company bonds are debt issued by firms and the cash they make by promoting them is to develop or increase into new enterprise traces or territories.

They have an inclination to pay larger charges of curiosity in comparison with authorities bonds, primarily due to the elevated threat of default.

Whereas bonds total are a low threat funding, company bonds are a greater choice for long run traders.

Quick Time period Funding Methods

With all the varieties of brief time period investments listed, you is likely to be confused and a bit overwhelmed as to what one of the best choices are for you.

Fortunately, I’ve you coated.

Here’s a breakout of brief time period funding methods you need to use proper now to earn extra curiosity with out a lot threat.

By following these methods, you’ll know precisely easy methods to make investments your cash.

#1. Begin Off With Excessive Yield Financial savings Accounts

It is advisable to have a cushion for emergencies and one of the best place for this cash is an account at your financial institution.

Whereas your wants could differ, I recommend retaining $10,000 on this account.

This permits for fast entry to your cash do you have to want it.

I notice saving $10,000 sounds intimidating, however you are able to do it.

Simply break it out into smaller targets, like saving $1,000 at a time and you’re going to get there quicker than you suppose.

Once more, I like to recommend going with CIT Financial institution since you may be incomes a wholesome quantity of curiosity in your financial savings.

After all, most any on-line financial institution will do, as most have a tendency to pay larger charge of curiosity than a conventional brick and mortar financial institution or credit score union.

Lastly, I like to recommend you could have a separate account for every of your financial savings targets.

This helps to maintain you motivated as you’ll be able to see the place you stand with every purpose.

#2. Create A CD Ladder

After you have $10,000 in financial savings on the financial institution, you’ll be able to start to create a ladder of CDs.

This works by having you put money into certificates of deposit which have completely different maturity dates and varied rates of interest.

By doing this you restrict the chance of rising charges whereas your cash is locked up.

I recommend you make investments your cash in 4 CDs with the next maturities:

- 12 Month (1 yr) CD: $1,500

- 18 Month (1 ½ yr) CD: $1,500

- 24 Month (2 yr) CD: $1,500

- 60 Month (5 yr) CD: $1,500

In complete you might be investing $5,500 in financial institution CDs. When every CD matures, you merely reinvest the cash for a similar time period in a brand new CD.

#2a. Make investments In Worthy Bonds

As a substitute for constructing a ladder with certificates of deposit, you’ll be able to put money into Worthy Bonds.

I encourage you to reap the benefits of their spherical up characteristic that can assist you pace up the method of saving cash shortly.

#2b. Make investments with Arrived

One other various to a CD ladder is Arrived.

You’ll get the next charge of return with a comparatively protected funding.

However you can not redeem your cash for six months and are charged a small price is you redeem earlier than 5 years.

The excellent news is that they have a minimal funding of simply $10.

#3. Spend money on Quick Time period Bond Funds

You now have $15,500 invested between financial savings and financial institution CDs or Worthy Bonds/Arrived.

The next move is investing briefly time period bond funds.

To do that, purchase the next bonds:

- iShares Quick Treasury Bond ETF: (SHV)

- iShares Extremely Quick-Time period Bond ETF: (ICSH)

- iShares 0-5 12 months Funding Grade Bond ETF: (SLQD)

You need to be sure to have the next share of every in your funding portfolio:

- 45% – iShares Quick Treasury Bond ETF (SHV)

- 35% – iShares Extremely Quick-Time period Bond ETF (ICSH)

- 20% – iShares 0-5 12 months Funding Grade Bond ETF (SLQD)

This can diversify your cash and give you a pleasant month-to-month earnings stream.

The draw back to that is each month your month-to-month earnings is getting taxed at strange earnings charges, which is larger than funding taxes.

So earlier than you do that, overview your monetary state of affairs to verify it is sensible for you.

Incessantly Requested Questions

There’s a number of confusion and a few thriller surrounding the numerous varieties of brief time period investments.

I created this FAQ part that can assist you perceive precisely what you might be moving into when investing in these funding varieties.

When ought to I put money into brief time period investments?

On the subject of investing, your time horizon performs an enormous position into what you really put money into.

With out making an allowance for your timeframe, you could possibly find yourself investing in an asset that’s too dangerous or one which carries too little threat and subsequently received’t present the return you want.

Due to this fact, it’s worthwhile to be sure to decide the correct funding primarily based on while you want the cash, your monetary targets, and threat tolerance.

Under is a chart in your reference.

| When Cash is Wanted | Greatest Funding |

|---|---|

| Much less Than 1 12 months | Money (Financial savings Account, CD) |

| Between 1-5 Years | Money & Quick Time period Bonds |

| Extra Than 5 Years | Shares & Bonds |

From the chart you’ll be able to see that if in case you have a short while horizon, corresponding to needing your cash in lower than 5 years, then you ought to be investing in money and/or bonds.

Investing in conventional long run investments like shares or equities at this level will not be suggested since you’ll threat dropping your principal in return for the next charge of return.

This threat is just too nice and it is best to stick to money and/or bonds.

Are brief time period investments protected?

The subsequent query I get requested concerning the various kinds of brief time period investments is are they protected.

For essentially the most half, they’re protected.

After all, should you pay attention to speak radio, there will probably be advertisements touting all kinds of protected investments, a lot of that are nowhere close to protected and others even I haven’t heard of.

Apart from these outliers, brief time period investments are protected to put money into.

Is my principal is protected?

The overwhelming majority of instances when investing in checking, financial savings, and certificates of deposits, the principal you make investments is protected 99.99% of the time.

The one means you’ll lose your principal is that if the financial institution the place the funding is held at goes below and it wasn’t coated by FDIC insurance coverage.

Moreover, should you had extra invested than the Federal Deposit Insurance coverage Company protection quantity permits, your additional financial savings may very well be in danger.

When do I threat dropping cash?

Regardless that these are protected investments within the sense you’ll by no means lose principal, relying on the rate of interest you might be incomes, you continue to threat dropping cash to inflation.

I’ve talked earlier than about inflation, however too many traders ignore it.

Over time, inflation eats away on the buying energy of your cash.

We see this on a regular basis.

I bear in mind as a child a pack of gum costing me $0.50. Now it prices $1.99.

That is the impact inflation has on costs. It causes costs to rise over time.

Traditionally, inflation runs between 2-3% yearly.

In case your financial savings account earns you 1% per yr, you might be dropping out to inflation.

Let’s have a look at the numbers to see this in motion.

Let’s say you could have $1,000 and need to use it purchase a house theater system that additionally prices $1,000.

However you don’t need to purchase it now, you need to purchase it in 1 yr after you could have your new home.

You determine to take a position your cash in a financial savings account incomes 1% yearly.

Throughout this time, inflation is operating at 3% yearly.

After one yr, you earned $10 in curiosity, making your financial savings value $1,010.

Due to inflation, the house theater system that price $1,000 at first of the yr now prices $1,030 on the finish of the yr.

Your financial savings account a protected sort of funding since you didn’t lose your authentic $1,000. However it isn’t a protected funding as a result of inflation is outpacing your return.

Whilst you earned $10 in curiosity, the price of the house theater system rose by $30, thus you “misplaced” $20.

That is the hazard of protected varieties of investments.

You sleep at night time as a result of you aren’t dropping the cash you saved or invested.

However you might be dropping buying energy and in consequence, want to save lots of more cash yearly.

That is why they name inflation the silent killer. It slowly destroys your funds behind the scenes.

The excellent news is that by incomes an rate of interest within the 2-3% vary, you retain tempo with inflation and it doesn’t have a unfavorable affect in your wealth.

Are there some other dangers with investing for the brief time period?

The one different threat elements is rate of interest threat.

As a result of charges can change, you threat not incomes sufficient cash to satisfy your purpose.

That is why it’s vital to take a position your cash in various kinds of brief time period securities to restrict this threat.

What are excessive yielding protected brief time period investments?

Sadly, there is no such thing as a such factor as a excessive yielding brief time period funding, no matter what the person on the radio or late night time tv is attempting to promote you.

At all times keep in mind that threat and return are associated.

The upper the chance, the upper the potential return you’ll be able to count on. The decrease the chance, the decrease the potential return you’ll be able to count on.

As of now, the best yield you’ll be able to count on to earn and nonetheless have your cash protected by way of not dropping cash is with Worthy Bonds or CIT Financial institution.

For my part, they’re one of the best brief time period investments you can also make and that is the place I put my cash.

The place is one of the best place to take a position my cash for 1 yr?

When you want your financial savings inside 1 yr, one of the best brief time period investing choices are a web based financial savings account or a financial institution or dealer CD.

The final word reply would be the rate of interest.

I decide these choices as a result of the chance of dropping cash is extraordinarily low and also you cash is FDIC insured.

I’d first take into account a web based financial institution since they’re straightforward to open and also you withdraw your cash at any time with out penalty.

Decide a couple of and see which one provides one of the best charges.

From there, I’d have a look at a couple of completely different banks for his or her charge on a 1 yr CD.

If the speed is larger than with a financial savings account, put money into the CD.

If the speed is decrease, then put your cash into an account with CIT Financial institution.

Is a Roth IRA a superb brief time period funding?

A Roth IRA is an effective place for a brief time period funding since you’ll be able to withdraw your contributions with none tax penalties or penalties.

You simply should make sure you solely are taking out as a lot as you invested.

It’s because whereas earnings are tax free if you’re over 59 ½ they’re topic to taxes and penalties should you withdraw them earlier than you flip 59 ½.

Additionally, you should definitely solely put money into much less dangerous investments.

This implies no shares should you count on to want the cash in lower than 5 years.

Ultimate Ideas

General, on the subject of the varieties of brief time period investments, you could have a handful of decisions.

Simply decide the correct funding automobiles for you targets and you ought to be all set.

Keep in mind to not fall sufferer of taking up extra threat only for the next return should you want the cash in lower than 5 years.

Belief me, the chance will not be value it.

Settle for that you’re incomes much less curiosity and be finished with it.

As you noticed from the numerous choices I listed, you’ll be able to nonetheless earn a good return with out taking up the added threat.

I’ve over 15 years expertise within the monetary providers trade and 20 years investing within the inventory market. I’ve each my undergrad and graduate levels in Finance, and am FINRA Collection 65 licensed and have a Certificates in Monetary Planning.

Go to my About Me web page to be taught extra about me and why I’m your trusted private finance skilled.